GST Blocked Credits Under Section 17(5) — What You Cannot Claim as ITC

Updated: 6 June 2026

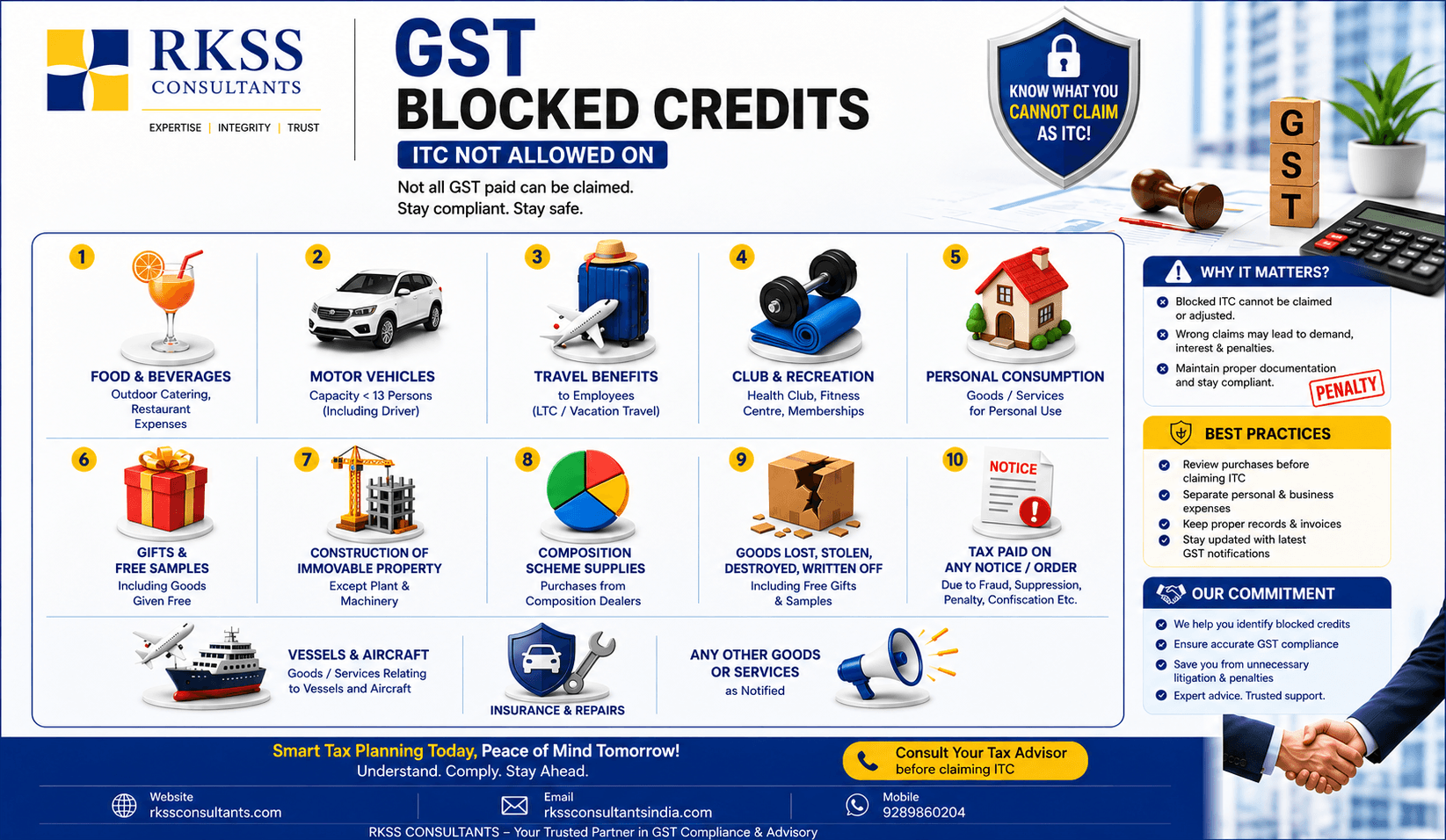

Not all GST paid can be claimed as Input Tax Credit. Section 17(5) of the CGST Act blocks ITC on specific goods and services. Know what you cannot claim and stay compliant.

What Are Blocked Credits?

Input Tax Credit (ITC) is one of the key benefits under GST — it allows businesses to offset GST paid on purchases against GST collected on sales.

However, Section 17(5) of the CGST Act, 2017 specifically blocks ITC on certain categories of goods and services, even if GST has been duly paid on them.

These are commonly referred to as "Blocked Credits" — and claiming them incorrectly can lead to demand notices, interest, and penalties.

13 Categories Where ITC Is Not Allowed

1. Food & Beverages — Outdoor catering, restaurant expenses, and food/drinks for employees.

2. Motor Vehicles — Vehicles with a seating capacity of less than 13 persons (including the driver), unless used for specific purposes like resale, transportation of goods, or passenger transport services.

3. Travel Benefits to Employees — Leave Travel Concession (LTC) and vacation travel provided to employees.

4. Club & Recreation — Health club memberships, fitness centre fees, and recreational facility expenses.

5. Personal Consumption — Goods or services used for personal consumption rather than business purposes.

6. Gifts & Free Samples — Goods given free of cost, including gifts and free samples distributed to clients or employees.

7. Construction of Immovable Property — Works contract services and goods used for construction of immovable property, except plant and machinery.

8. Composition Scheme Supplies — Purchases made from composition dealers are not eligible for ITC.

9. Goods Lost, Stolen, Destroyed or Written Off — Including free gifts and samples covered under this category.

10. Tax Paid on Any Notice or Order — GST paid due to fraud, suppression, penalty, confiscation, or any other enforcement order.

11. Vessels & Aircraft — Goods or services related to vessels and aircraft, subject to certain exceptions.

12. Insurance & Repairs of Ineligible Motor Vehicles — Insurance, repair, and maintenance of motor cars and vehicles that are themselves ineligible for ITC.

13. Any Other Goods or Services as Notified — Any additional categories notified by the government from time to time.

Why This Matters for Your Business

Blocked ITC cannot be claimed or adjusted against your GST liability — treating it as eligible ITC is a compliance violation.

Wrong claims may lead to demand notices, interest at 18% per annum, and penalties up to 100% of the tax amount in cases of fraud.

Maintaining proper documentation is essential — even for expenses that appear business-related, you must verify whether they fall under Section 17(5).

Regular review of purchase invoices before filing GSTR-3B is strongly recommended to avoid inadvertent claims.

Best Practices to Stay Compliant

Review all purchase invoices before claiming ITC in your GST returns.

Clearly separate personal and business expenses in your books of accounts.

Maintain proper records and invoices for all ITC claimed, including the nature and purpose of each expense.

Stay updated with the latest GST notifications, circulars, and amendments as the list of blocked credits can be modified.

Consult a GST advisor before claiming ITC on borderline expenses — especially motor vehicles, construction-related costs, and employee welfare expenses.

Need Professional Assistance?

If you have questions regarding GST compliance, ITC eligibility, corporate governance, or any other tax and regulatory matters, our team can help you navigate the latest requirements and ensure full compliance with applicable laws.